The Quantum Economic Development Consortium (QED-C) held its 2026 Quantum Technology Showcase on Capitol Hill on July 16, 2026, drawing senior administration officials, bipartisan Congressional staff, and senior staff from IBM Research, Google Quantum AI, Quantinuum, Rigetti, and Infleqtion. The event followed the July 2025 White House Summit on American Quantum Innovation and a series of executive orders directing federal coordination on quantum R&D, supply-chain security, and workforce development.

Live demonstrations spanned quantum computing hardware, quantum sensing, quantum communications, and enabling subsystems such as cryogenics, control electronics, and photonics. Discussions with members of Congress focused on supply-chain resilience, NIST standardization timelines, and pathways to scale commercial applications under the renewed National Quantum Initiative.

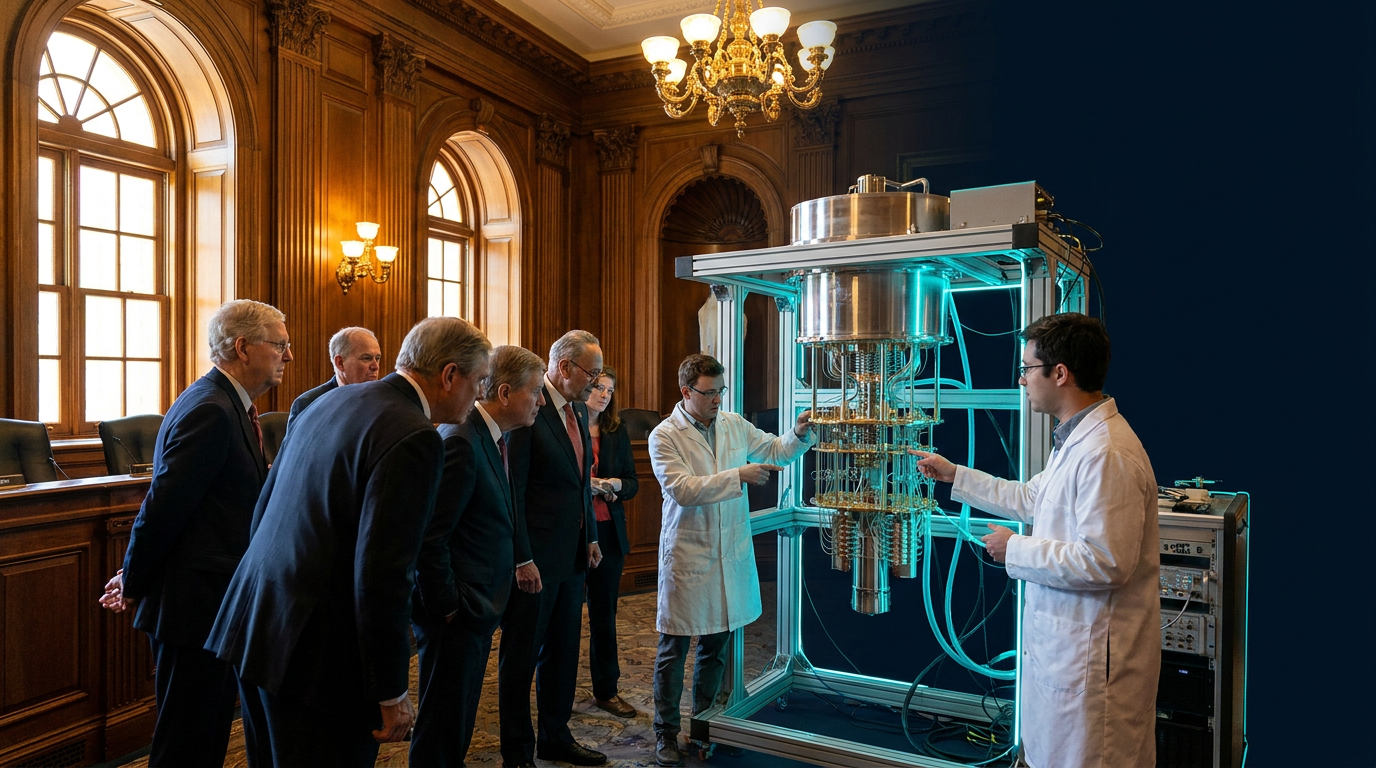

What the Showcase Actually Showed

Live, in-room demonstrations. That is the substantive fact. QED-C staged physical systems on Capitol Hill rather than slideware, with booths from IBM (superconducting transmon and Heron-class processors), Google Quantum AI (Willow-class superconducting with surface-code logical qubit milestones), Quantinuum (trapped-ion H-series systems with claimed 99.9%+ two-qubit gate fidelity), Rigetti (Ankaa-class superconducting), and Infleqtion (cold-atom Sqorpius platform for sensing and timing).

No peer-reviewed hardware benchmark was released at the event itself. What was released was access: policymakers handled dilution refrigerators, spoke with control-systems engineers, and saw quantum-sensing prototypes targeting inertial navigation (a known DoD interest area after the 2024 NDAA quantum-sensing provisions). The signal is bilateral: industry acquired face time with appropriations staff ahead of the FY2027 funding cycle; Congress acquired baseline literacy on error correction, logical qubit counts, and the difference between NISQ-era heuristics and fault-tolerant roadmaps.

Winners and Losers

Winners from the policy backdrop. The 2026 National Quantum Initiative reauthorization — pending markup as of July 2026 — would lock in multi-year funding for DOE, NSF, and NIST quantum programs at a reported aggregate level of roughly $2.7 billion over five years. Companies with deep federal contracting lanes — IBM, Google (with its Mountain View and Santa Barbara labs), and Quantinuum — benefit most directly because their commercialization timelines depend on sustained government offtake and standards work.

Losers from the protectionist framing. The showcased rhetoric on supply-chain resilience, particularly regarding rare-earth isotopes, cryogenic components, and dilution-refrigerator manufacturing, signals procurement preference for domestic or allied suppliers. Origin Quantum, IBM's Chinese counterpart, and any quantum-hardware startup reliant on restricted components face tighter access. Photonics and cryogenics suppliers (Bluefors, Lake Shore Cryotronics, Quantum Machines) become the second-order winners, as their order books track federal and prime-contractor demand.

Threatened: the gap between policy ambition and commercial revenue. Quantum computing remains pre-profit at scale for the majority of named players. IonQ reported $43.1 million in 2025 revenue; Rigetti reported $10.8 million; both are sub-scale relative to R&D burn. Sustained federal support cushions but does not close that gap. If Congressional appropriations soften in FY2027 or FY2028, runway compresses fastest for the publicly traded pure-plays.

The Bigger Picture

Capitol Hill showcases are a recurring feature of the U.S. quantum policy calendar; the Innovation showcase follows the September 2025 White House summit that re-anchored quantum as a national-security priority. By mid-2026, the executive orders signed in late 2025 — covering export controls on quantum-relevant cryogenics and quantum-specific EAR/BIS rules — are in force, and the CHIPS-and-Quantum analogy has become standard Hill shorthand.

For calibration: the EU Quantum Pact, signed in March 2026, commits €1.2 billion to the Quantum Flagship successor program through 2030. The UK National Quantum Technologies Programme is in its fourth tranche, with £2.5 billion announced for 2025–2030. China's reported central-plus-provincial quantum spend remains opaque but is independently estimated at well above $4 billion annually. The U.S. policy package is competitive, not dominant, on absolute quantum spend; its edge is procurement concentration, not budget dominance.

The Signal

The signal here is that quantum is no longer fighting for legislative attention — it is now defending budgets against sequestration and intra-science reshuffling. The technical claim worth tracking is whether any of the showcased systems crosses a published, peer-reviewed threshold of fewer than one logical error per million physical operations on a code-distance surface code, the IBM/Google fault-tolerance benchmark that the community treats as the next inflection. No demonstration at the Capitol Hill event cleared that bar; the closest publicly stated milestone remains Google Quantum AI's Willow announcement from December 2024, with below-threshold error suppression demonstrated at distance-7. Until that bar moves, the policy momentum is real and the commercial inflection is not.

The 2026 QED-C Capitol Hill showcase converted a year of executive orders into legislative momentum, but the industry's commercial inflection still hinges on a fault-tolerance benchmark no system has yet cleared.

In short: QED-C's 2026 Capitol Hill quantum technology showcase demonstrated systems to lawmakers, validated the policy pipeline from the 2025 White House quantum summit, but did not move the underlying fault-tolerance benchmark that determines enterprise adoption timelines.