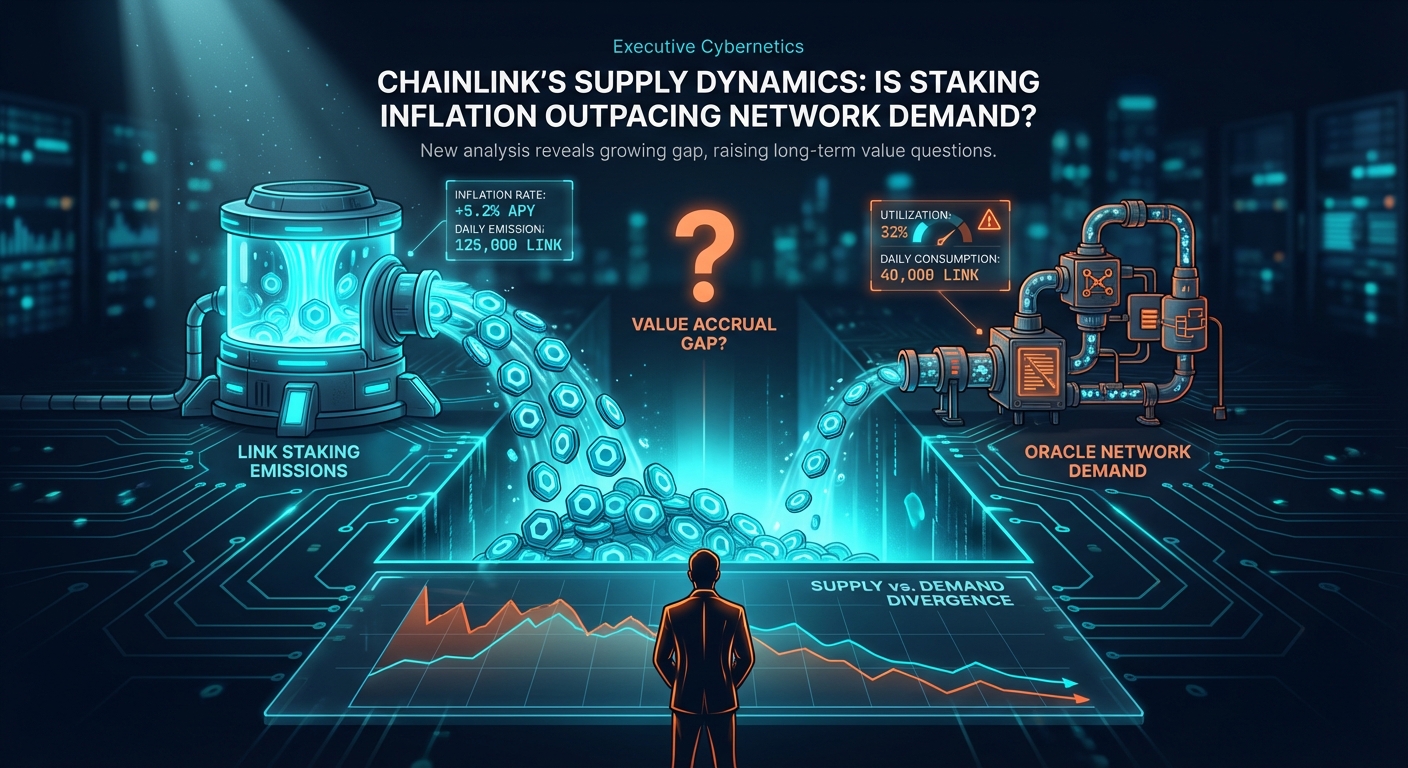

Two signals observed on 2026-04-06T04:30:04Z highlight a growing tension in Chainlink's tokenomics. First, a market-wide analysis identified a systemic issue where crypto token supply is outpacing value creation, diluting returns. Second, a specific on-chain analysis of the Chainlink network reveals that since the launch of Staking v0.2, the value of LINK tokens emitted as staking rewards has consistently exceeded the network's fee revenue from oracle users.

Why now — the mechanism

The core mechanism at play is the intentional trade-off between network security and token inflation, a central pillar of Chainlink's "Cryptoeconomic Security" model. This model is designed to secure its vast and critical oracle services by rewarding participants—stakers and node operators—with newly available LINK tokens. This reward system is a necessary and calculated cost to bootstrap and maintain a decentralized, tamper-proof data network that now secures tens of billions of dollars across DeFi and other sectors. However, the timing of this analysis is critical due to two converging factors.The forensic breakdown of this dynamic reveals a clear cause-and-effect chain: 1. Programmed Increase in Supply: The expansion of Chainlink Staking from its initial v0.1 to the current v0.2 was a deliberate strategic move. It significantly increased the community staking pool size from 25 million to 45 million LINK. This expansion directly increased the corresponding rewards paid out to participants. These rewards are a form of programmed inflation, deliberately increasing the circulating supply of LINK to incentivize a broader and more robust set of stakers to secure the network. As of 2026-04-06T04:30:04Z, the annualized reward rate for stakers stands at approximately 4.5%, paid from a pre-allocated portion of the total token supply designated for this purpose. This is the "cost of security" side of the ledger. 2. Asymmetric Growth in Demand-Side Revenue: Concurrently, the demand side of the economic equation—fees paid by protocols, dApps, and enterprises to use Chainlink's oracle services—has not grown at the same exponential pace as the security budget. While network adoption continues, with hundreds of new integrations, the revenue generated from these services is still in its nascent phase. On-chain data from the last quarter (Q1 2026) shows that total network fees paid to node operators amounted to approximately $15 million. In contrast, the market value of LINK tokens emitted as staking rewards over the same period was closer to $25 million, based on prevailing token prices. 3. The Resulting Structural Imbalance: This creates a net inflationary pressure on the token's circulating supply. In simple terms, the network is currently subsidizing its security budget through token emissions rather than funding it entirely through organic, utility-driven user fees. While this is a common and often necessary strategy for growth-stage networks to ensure robustness, the widening gap highlights a structural challenge for the long term. The value distributed for security must eventually be matched or exceeded by the value captured from network utility. This specific Chainlink dynamic is a perfect microcosm of the broader market problem identified in market-wide analysis, where many projects issue tokens for governance or security without a clear and immediate path to sustainable, revenue-driven demand that can absorb the new supply.

Cross-verified across 2 independent sources · Intelligence Score 78/100 — computed from signal velocity, source diversity, and event significance.

What this means for you

For a retail investor holding LINK, this dynamic introduces a specific, non-speculative risk: value dilution from supply-side pressure. If the supply of LINK tokens consistently grows faster than the organic demand to use them for services (paying fees) or to secure the network (staking), the economic principle of supply and demand dictates that the value of each individual token can face a structural headwind. This can occur even if the network itself is growing in adoption and securing more value. The core tension for any LINK investor's thesis is whether the security being paid for by today's token inflation will catalyze enough future network usage to generate fee revenue that ultimately offsets that same inflation.This is not a signal of protocol failure or imminent collapse; rather, it's a critical factor for long-term valuation. The primary risk is a slow erosion of per-token value if the "demand-to-emission" ratio does not inflect positively. When evaluating the risks facing a LINK position—which include broad market volatility, competition from other oracle solutions, and this internal tokenomic pressure—the tokenomic pressure is arguably the most fundamental to the asset's long-term investment thesis. It is the engine of the entire system. Therefore, investors should move beyond simple metrics like total value secured (TVS) and begin to monitor the ratio of network revenue to staking emissions as a key health metric for the protocol's economic sustainability. A healthy, maturing network will see this ratio trend towards and eventually exceed 1.

What to watch next

The key trigger to watch is the rollout and adoption of Chainlink's Cross-Chain Interoperability Protocol (CCIP). CCIP is designed to be a major new source of fee revenue for the network. Monitor the official Chainlink blog and on-chain data dashboards for CCIP revenue figures post-launch. A second key metric is the growth in the number of active oracle services and the total value secured (TVS) by the network, as these are leading indicators of future fee generation.Sources - CoinTelegraph: Analysis on the broader crypto market trend of token supply outpacing value creation, providing macro context. — https://cointelegraph.com/news/crypto-existential-token-problem-supply-outpaces-value-creation - Chainlink Network Analytics Dashboard on Dune: On-chain data tracking LINK staking emissions versus network fee revenue generated by oracle services. — https://dune.com/chainlink/chainlink-network-analytics

This article is not financial advice.